Supply chain & Logistics in Australia and New South Wales

Industry conditions and the labour market in 2026

Australia's logistics sector is growing, but what increasingly limits that growth is the availability of skilled people rather than a shortage of demand. This report looks at the national sector and the New South Wales market, and at how the main forces reshaping the industry, online retail, automation, the move to low-emission fleets and a wave of new freight infrastructure, are changing what operators need from their workforce. Clear trends shaping the future of the industry is that the work of supply chain professionals is becoming more technical, suitable candidates are getting harder to find, and the operators best placed to grow are the ones that can attract and keep skilled staff.

1. Sector overview

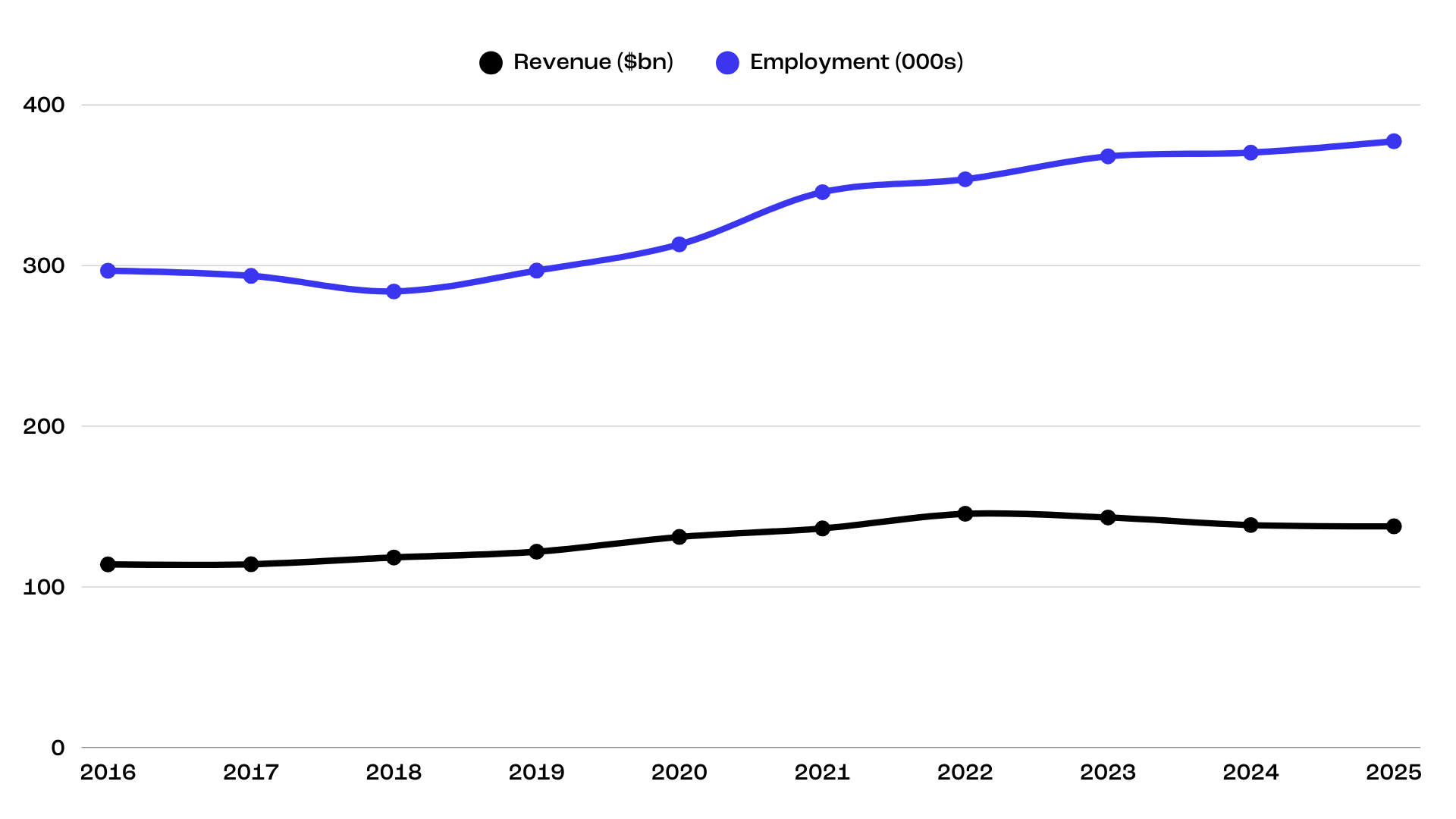

Australia's integrated logistics sector earned $137.7 billion in revenue in 2024-25 and employed 377,417 people across roughly 114,000 businesses. The sector covers the third-party movement and storage of goods, including road, rail, air and sea freight, postal and courier services, freight forwarding, warehousing and distribution. It does not include bulk commodity freight or passenger transport. Once passenger transport is added, the wider Transport, Postal and Warehousing industry employs around 745,000 people, which makes it one of the largest sources of jobs in the country. The sector's share of the economy has been growing faster than the economy as a whole, driven by population growth and the rising volume of goods Australians buy and move.

Growth over the past five years has been slow on average, at about 1% a year, but that average hides a sharp cycle. Online demand pushed revenue up strongly in 2019-20 and again in 2021-22, after which revenue fell for three years running as pandemic-era buying returned to normal and a downturn in construction cut demand for moving building materials. Revenue is expected to recover from here, growing at about 2% a year to reach $152.1 billion by 2029-30.

The more telling number for anyone hiring in this sector is employment, which has held up far better than revenue. The workforce grew from 313,199 in 2019-20 to 377,417 in 2024-25 and is forecast to reach 436,372 by 2030-31. Headcount kept rising even while revenue was falling, because the sector's growth is driven by the volume of parcels and orders it handles, and that volume keeps climbing regardless of the revenue cycle. The number of businesses grew over the same period, from around 86,000 to 114,000.

The market is crowded and competition is strong. The four largest operators, Australia Post, Toll Holdings, Linfox and Mainfreight, together hold only about 12.6% of revenue, with Australia Post the largest at just 6.9%. The remaining 87% is shared among thousands of mid-size and smaller operators. It is becoming harder for newcomers to compete, because the technology and equipment now needed to win work favour larger, better-funded operators. This is slowly pushing the sector toward consolidation, with bigger operators buying smaller ones to extend their reach and capability.

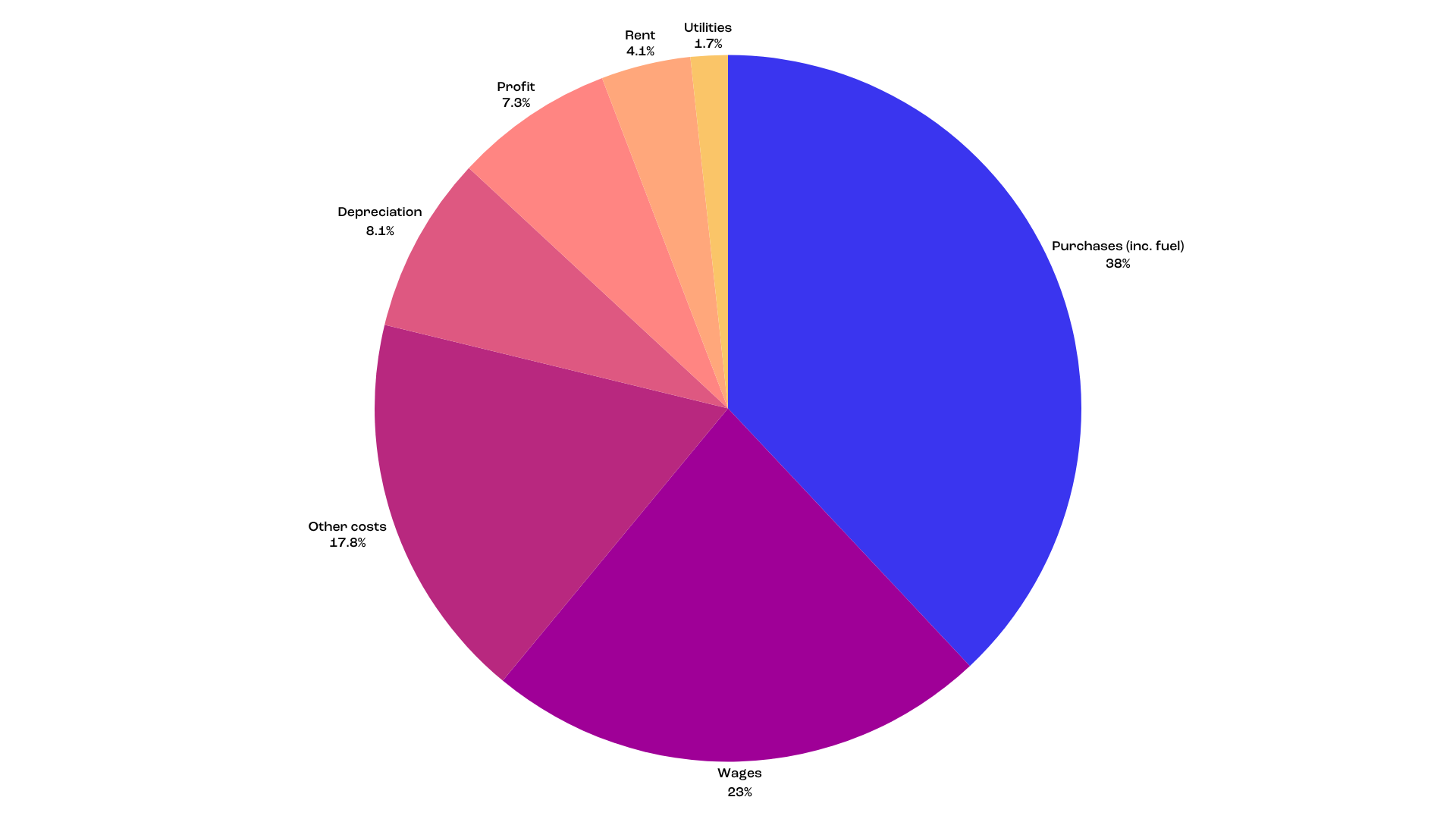

Profit margins are thin, which makes the sector sensitive to its costs. It earned $10.1 billion in profit in 2024-25, a margin of 7.3%, which has improved slightly over five years as larger operators added higher-value services such as data tracking and analytics. The biggest cost is purchases, dominated by fuel, at about 38% of revenue. Wages are next at 23%. Because fuel and wages together make up most of the cost base, anything that moves fuel prices or wage rates flows quickly through to profitability, which is why operators lean so heavily on fuel surcharges, automation and more efficient vehicles to protect their margins.

Sources: IBISWorld (Integrated Logistics in Australia, June 2025) and Jobs and Skills Australia.

2. The forces reshaping demand for skilled labour

Four forces are changing what logistics operators need from their workforce. They are the growth of online retail and the shift to road freight, the spread of warehouse automation, the move to low-emission fleets, and the pressure of fuel and other costs. Each pushes demand toward more technical, systems-based roles and away from purely manual work. This section looks at what is driving demand for labour. Section 3 looks at whether the supply of workers can keep up.

2.1 E-commerce and the shift in freight demand

Online retail is the main engine of growth. Retailers, and online sellers in particular, are the sector's largest customers at 38.4% of revenue, ahead of manufacturers at 27.9% and wholesalers at 27.7%. The move to online shopping that began during the pandemic has held, which means more parcels to move and more complex orders to fulfil. Operators have responded by offering complete order-to-doorstep services that combine warehousing, stock management, order processing and final delivery. Running these services well takes more technical skill than traditional freight work.

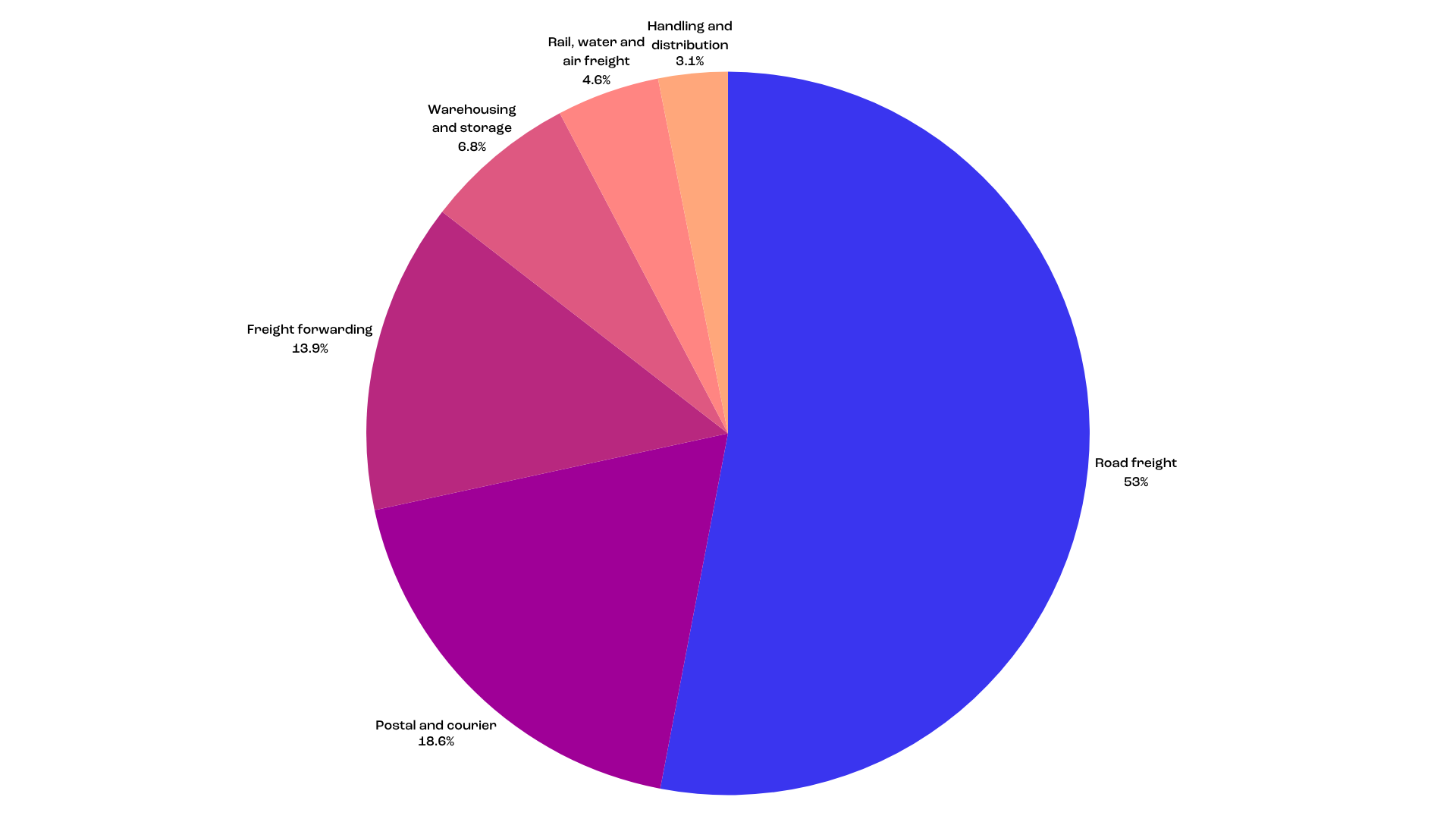

Road freight is still the largest part of the sector at 53% of revenue, with postal and courier services second at 18.6%. These figures show where the money sits today, but they understate how fast the balance is shifting.

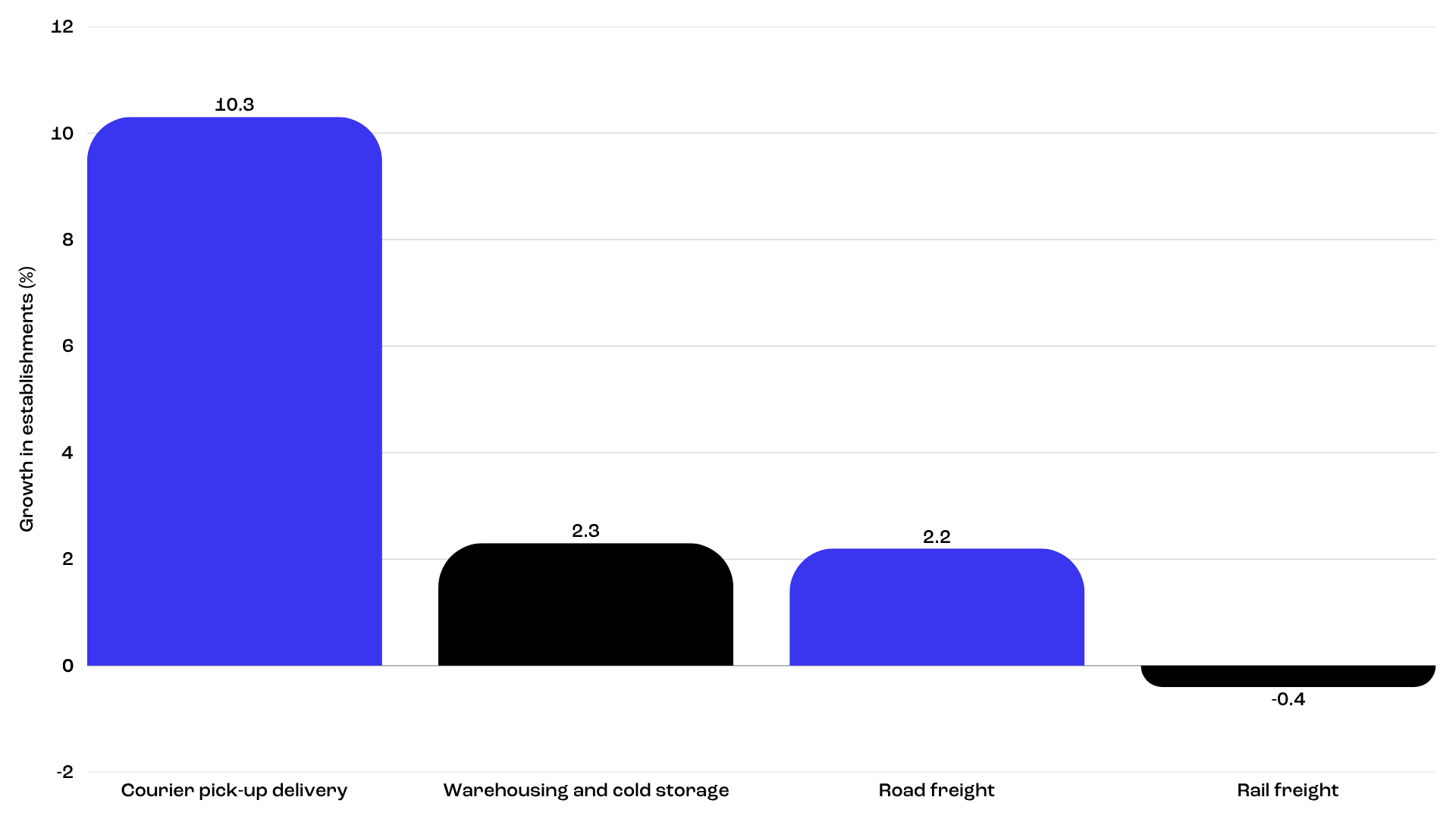

The number of courier and parcel-delivery businesses is growing far faster than any other part of the sector, while rail freight is shrinking. The reason is structural. The goods online retail generates, smaller and time-sensitive parcels rather than bulk loads, suit the flexibility of road and parcel networks, while rail stays tied to bulk commodities such as coal and iron ore. This shift has a long runway, with road freight volumes expected to grow by around 77% between 2020 and 2050, against just 5.7% for rail. For employers, it means steady demand not only for drivers but for the planners and systems operators who keep increasingly complex parcel networks running.

2.2 Automation, robotics and AI in the warehouse

Automation is the force changing the workforce most, and it is led by the larger operators that can afford the upfront cost. The examples are recent and large. Coles spent around $880 million on a fully automated distribution centre at Truganina in Victoria. Linfox runs automated storage and retrieval systems, robotic palletisers and automated guided vehicles, and has worked with the software firm SAP to automate stock management across three warehouses. DHL began automating its healthcare warehouses in late 2024.

These investments change the mix of jobs on the warehouse floor. Manual picking and lifting give way to operating, monitoring and maintaining the machines. The effect on pay is already visible in job ads, with automation operator roles advertised at base salaries between $90,177 and $137,861, well above what a traditional warehouse hand earns, because the work needs people who can run control systems rather than move stock by hand. Automation also raises spending on equipment and reduces errors and the need for manual labour, which is part of why the larger operators held their margins steady through the recent soft patch in revenue.

Because automation is expensive, it stays concentrated among the operators that can fund it, which widens the gap between advanced firms and smaller ones. Driverless trucks would extend this trend, but safety and regulatory hurdles mean any real change in demand for drivers is still years away.

2.3 The move to low-emission fleets

The national push toward net zero is speeding up the switch to electric trucks, and again the larger operators are moving first. With support from the Federal Government's Driving the Nation program, Toll and Linfox announced in late 2024 that they would put 28 and 26 battery-electric trucks into service, with Toll's commitment worth around $67 million once charging infrastructure is included. Operators that cannot afford to make the switch face higher running costs over time as customers increasingly favour low-emission delivery.

The switch is also creating a shortage of the right mechanics. Fewer than one in ten mechanics is currently qualified to work on electric vehicles, which limits how quickly fleets can be serviced and adds electric-vehicle maintenance to an already long list of hard-to-find skills.

2.4 Fuel and cost pressures

Fuel is the sector's biggest outside risk. High oil prices in recent years lifted transport costs across the board, with road and last-mile delivery hit hardest. Operators have mostly protected their margins by passing fuel costs on to customers through surcharges built into contracts.

The bigger risk for employment is indirect. If fuel-driven inflation pushes up the cost of living for long enough, households spend less on non-essential items, and that would soften the online retail demand that drives parcel hiring. This is a possible downside rather than the most likely outcome, and the easing of Middle East tensions through 2026 has made it less of a near-term concern. The sector also has a natural buffer, because it serves a wide spread of customers across retail, manufacturing, wholesale and agriculture, so a downturn in any one of them does limited damage on its own.

Sources: IBISWorld (Integrated Logistics in Australia, June 2025, and From Fuel Pumps to Farm Gates, May 2026), Australian Department of Infrastructure, Australian Logistics Council and SEEK.

3. A higher skill bar meets a tighter supply of workers

The people who move and store Australia's goods are part of the broader Transport, Postal and Warehousing workforce, which numbers around 745,000 and grew by about 2% in the year to February 2026. It is an ageing and largely male workforce, with a median age of 43 and women making up just 22%. Truck drivers are the single largest occupation, followed by warehouse storepersons, delivery drivers, couriers and forklift operators. Above this operational base sits a smaller but fast-growing layer of professionals, including supply chain planners, distribution and procurement managers and logistics analysts. Median full-time pay across the whole industry is $1,608 a week, below the all-industries median of $1,741, a figure held down by the large number of entry-level delivery and warehouse roles.

Official projections have employment growing by about 9% over the decade to 2035, below the 13% expected across all industries. That number understates the real pressure for two reasons. The first is that it leaves out the effect of automation and AI, which the projections do not attempt to capture and which will reshape the mix of roles. The second, and more important for employers, is that it is an average that hides acute shortages in exactly the roles the sector most needs.

The clearest shortage is in heavy-vehicle drivers, where the workforce is short by an estimated 26,000 and nearly half of current drivers are over 55, even as the road freight task is set to grow by around 11.5% over five years. The shortage extends to the technical trades and professions that keep modern logistics running. There are close to 3,000 unfilled heavy-vehicle mechanic roles, fewer than one in ten mechanics can service electric vehicles, and operators report critical gaps in logistics and distribution managers, supply chain planners and data and IT specialists. These roles cannot be filled quickly, because they depend on training and experience that take years to build.

Pay reflects where the scarcity lies. According to our salary data, truck drivers typically earn between $70,000 and $100,000, while transport and fleet managers earn $125,000 to $155,000. In the professional roles that clients increasingly compete for, supply chain analysts earn $80,000 to $97,500 and reach $100,000 to $130,000 with demand-planning or systems experience, supply chain managers earn $125,000 to $145,000 and well above $195,000 at national level, and procurement managers earn $135,000 to $160,000. Sydney pay runs 7–12% above the national average. The largest premiums go to candidates who pair operational knowledge with technical skills such as SAP or Oracle systems, Power BI or Tableau reporting, demand forecasting and inventory optimisation. The pattern is consistent across every source. Pay is climbing fastest where skilled, systems-capable people are hardest to find, and the sector-wide average understates this because it is pulled down by the rapid growth of lower-paid last-mile parcel roles.

Sources: Jobs and Skills Australia, Australian Logistics Council, Industry Skills Australia, and IBISWorld.

4. New South Wales and the Western Sydney engine

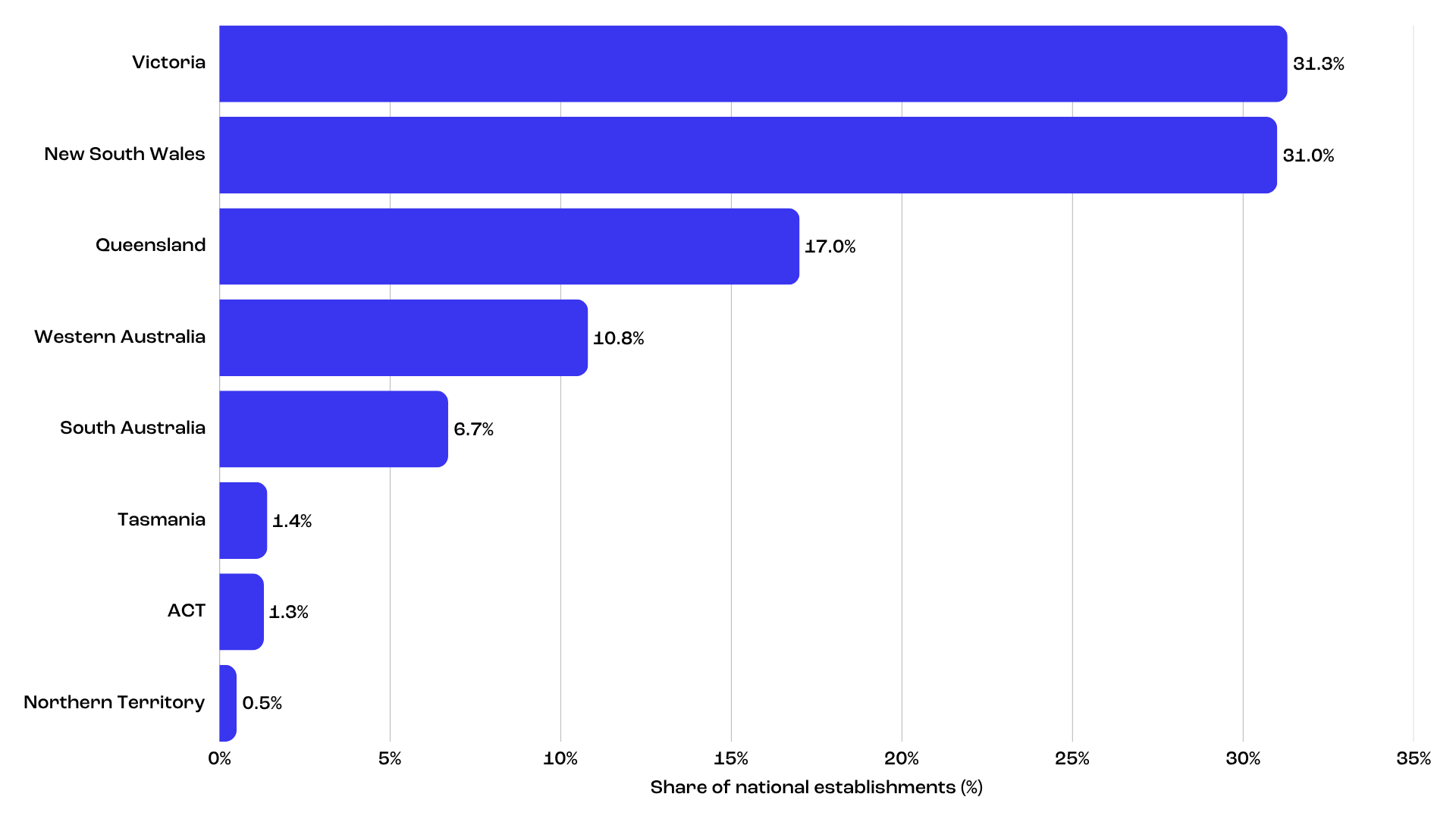

New South Wales is the second-largest base for logistics operators in the country, home to around 31% of the sector's establishments, just behind Victoria. Together with Victoria and Queensland it accounts for roughly 80% of all operators and about three-quarters of national freight volumes, a concentration that follows the population and port infrastructure of the east coast. Sydney's position is anchored by Port Botany, which draws operators specialising in imports, customs and container handling, and the Sydney basin alone handles close to half of Australia's air freight.

What sets New South Wales apart over the next decade is the scale of new freight capacity being built, most of it in Western Sydney. Western Sydney International Airport opens in 2026 and is expected to support close to 28,000 direct and indirect jobs by 2031. Nearby, the Moorebank Logistics Park, the country's largest intermodal precinct, is estimated to create up to 6,800 ongoing jobs once fully operational, across warehousing, transport, terminal operations and site management, on top of around 1,300 construction roles. A further Western Sydney freight line and intermodal terminal is in planning with Transport for NSW. Private investment is following the same path, with Toll committing $420 million to a Western Sydney warehouse and the property group ESR holding a $300 million logistics development site in the region.

These projects matter for employers because of the kind of work they create. An intermodal terminal and an automated airport cargo operation need people who can run and maintain control systems, coordinate freight across road and rail, and manage customs and forwarding, not manual labour alone. Roles advertised at the new airport already call for skills such as PLC and SCADA control-system experience to monitor automated baggage and cargo systems. The largest concentration of new logistics jobs in the country is forming in Western Sydney, and it leans toward exactly the technical and supervisory roles that are already in short supply nationally.

Sources: IBISWorld, Western Sydney Airport, Moorebank Intermodal Company (Deloitte, 2016), Transport for NSW, Mordor Intelligence and SEEK.

5. Outlook, implications and recommendations

The demand outlook is positive. Revenue is forecast to reach $152.1 billion by 2029-30 and the workforce to grow to around 436,000 by 2030-31. Several forces support this. A growing population buys more groceries and household goods, which lifts road freight and warehousing. A stronger Australian dollar makes imports cheaper, encouraging retailers and wholesalers to hold larger inventories and increasing demand for warehouse space. Strong agricultural exports keep specialist and refrigerated transport busy. And the Federal Government's target of 1.2 million new homes by 2028-29 points to a recovery in construction freight after several weak years. Major public investment in roads and in the Melbourne to Brisbane Inland Rail reinforces the trend.

At the same time, the sector is consolidating. Larger, technology-enabled operators are pulling ahead of smaller ones that cannot fund automation and electric fleets, and investor appetite for logistics assets is strong. The clearest recent example is the agreed $11.7 billion take-private of Qube Holdings, one of the country's largest logistics and port operators, by a Macquarie-led consortium in early 2026. Smaller operators are more likely to be acquired than to compete head-on.

The common thread across this report is that demand is not the main constraint on the sector's growth. Skilled labour is. The work is becoming more technical through automation, the move to electric fleets adds scarce trades, and the largest block of new capacity, in Western Sydney, is weighted toward technical and supervisory roles. The operators best placed to capture the coming growth will be those that can attract, develop and keep skilled people. This is not a new idea to the sector itself, which ranks securing a skilled workforce among its most important success factors.

For employers, several priorities follow. Workforce planning is better treated as a growth lever than a back-office task, with driver and trade pipelines built now given an ageing workforce and weak training intake, supported where appropriate by skilled migration. Reskilling existing staff toward automation, control-system and data roles is often faster and more reliable than competing for a thin external market. Because experienced professionals are willing to move and pay is rising, retention, career pathways and reputation as an employer matter as much as salary, and pay is best benchmarked against the technical skills that now command a premium. Operators expanding into Western Sydney should secure technical and supervisory talent early, ahead of the airport ramp-up. For the scarcest roles, the market is now too tight to leave to chance, and a targeted, specialist approach to finding and assessing candidates is increasingly what separates operators that fill critical positions from those that leave capacity standing idle.

[Insert Figure 6. priorities ]

Sources: IBISWorld (Integrated Logistics in Australia, June 2025), Australian Department of Infrastructure and company disclosures.