Danijela Negro • April 16, 2026

New ABS Data Released Today: Key Insights

Q1 2026 Australian Labour Market Update

Supply Chain & Logistics | Finance & Accounting | Business Support

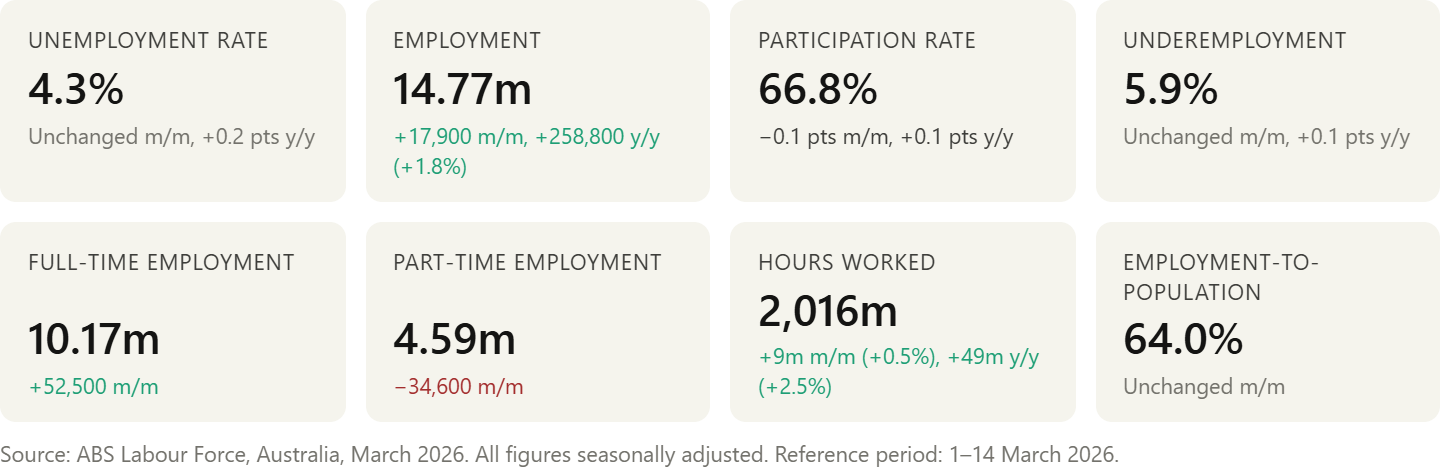

Australia's first quarter closed with unemployment steady at 4.3% and employment at a record high of 14.77 million. The headline story is continuity rather than change. Participation, underemployment, and the employment-to-population ratio all held close to where they have been for much of the past year.

The quarter was not without complication. The Iran conflict, which began at the end of February, introduced energy price volatility and global shipping disruption during March. Business and consumer confidence indicators moved sharply in response, though labour market figures typically lag such shocks by several months. The full flow-through to hiring activity will not be visible until later in 2026.

This update examines where the market stands after Q1 and what the data suggests for workforce planning across supply chain and logistics, finance and accounting, and business support.

Employment at a glance

Macro Trends

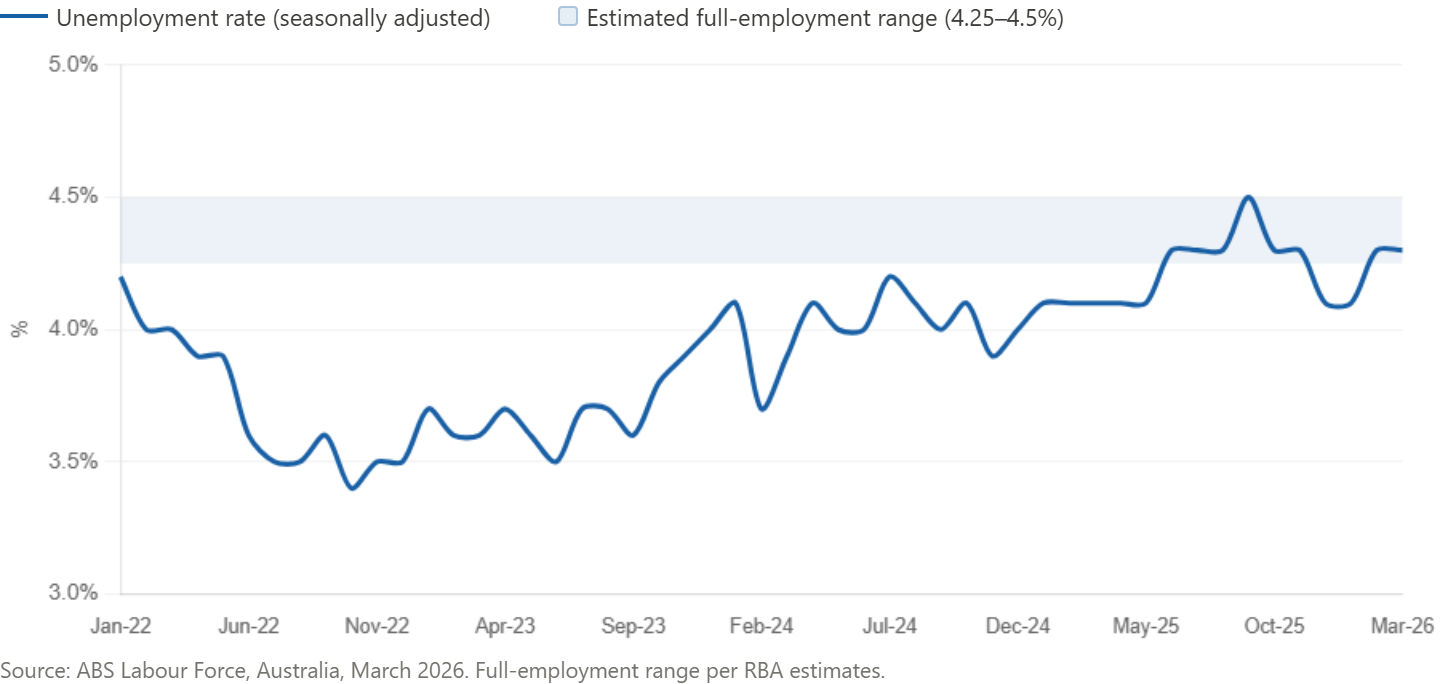

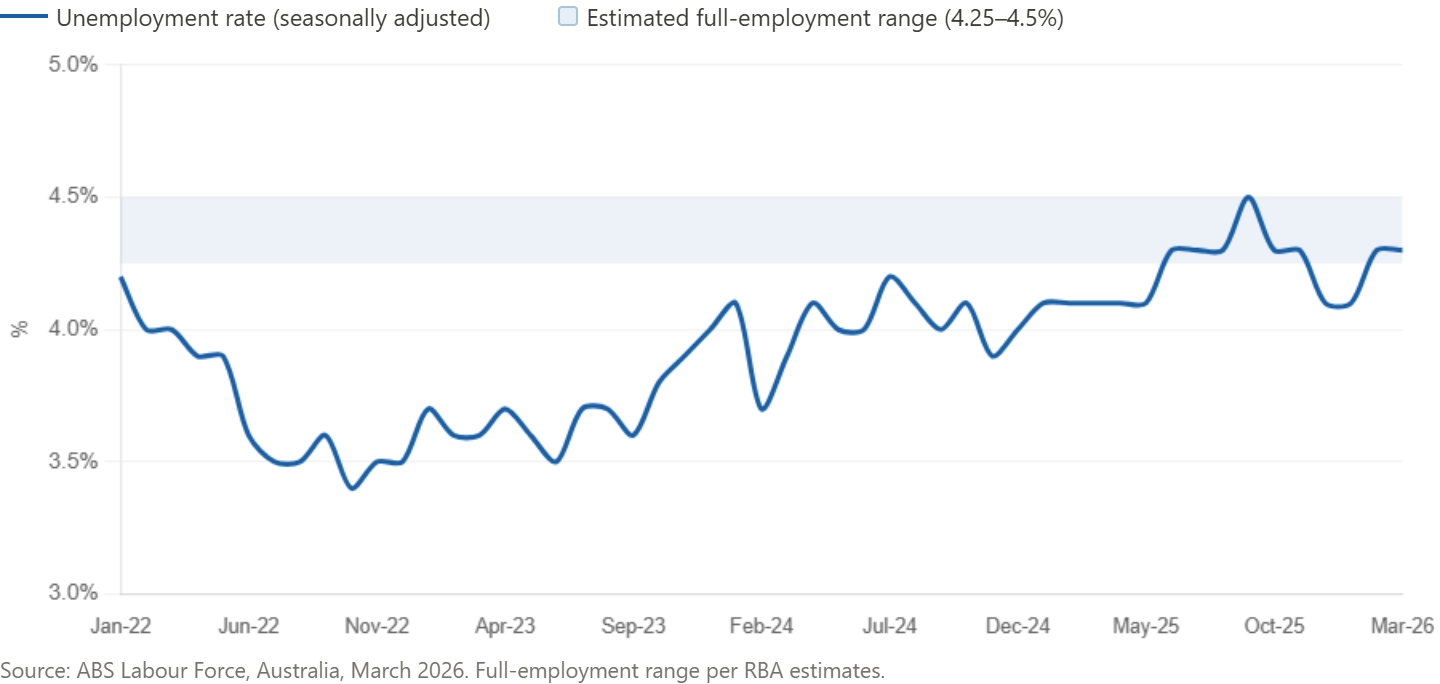

Unemployment has settled into a narrow range

Unemployment has now held between 4.1% and 4.3% for the whole of Q1. Before that, it drifted gradually upward from post-pandemic lows near 3.5% in mid-2022. The RBA has previously described this range as broadly consistent with full employment, meaning the labour market is tight enough to absorb most available workers but not so tight that wage pressure becomes acute.

What the rate looks like in practice is a market that has finished most of its post-pandemic rebalancing. The intense competition for staff that defined 2022 and 2023 has eased, but unemployment remains low by any historical measure. March is the first month where the reference period overlaps with the Iran conflict, and no dislocation is yet visible in the data. Because employment figures lag demand shocks, the read across to hiring activity will take two or three months to fully surface.

The practical takeaway for employers is that headline hiring conditions look stable, but the environment influencing next quarter's decisions has shifted. Experienced candidates in specialist roles continue to move slowly through the market, and the competition to secure them is comparable to what it was a year ago.

Month-to-month composition is unusually volatile

Q1 produced unusually volatile month-to-month movements within the overall employment figures. February saw full-time employment fall by 30,500 while part-time rose 79,400, a pattern that suggested employers were hedging toward flexible capacity. March reversed almost exactly, with full-time adding 52,500 positions and part-time falling 34,600. Over the two months combined, the net picture is a small tilt toward part-time work, but the pattern is considerably choppier than any single month indicates.

Several factors are likely behind the swings. Some employers facing cost uncertainty have been cycling capacity through part-time and contract roles before committing to permanent hires. Others have been converting probationary arrangements into full-time positions as they gain confidence in the fit. The broader signal is that hiring intent remains positive, but firms are making their commitments month by month rather than quarter by quarter.

This has a practical implication for how recruitment is approached. When individual engagements carry more weight, the accuracy and fit of each hire becomes more commercially significant. There is less room to bring someone on and develop them slowly into the role, and the premium on candidates who can contribute from the first week has grown. For sectors already facing skills scarcity, this means the competition for experienced candidates is running at a higher intensity than the headline figures would suggest.

Hours worked are growing faster than employment

The March data also shows hours worked rising ahead of headcount. Monthly hours across all jobs grew 0.5% in March compared with employment growth of 0.1%, and over the past year hours are up 2.5% against employment growth of 1.8%. The gap has been widening steadily since late 2025.

The pattern is consistent with what typically happens when employers become more cautious about hiring. Existing staff take on more work, either through extended hours or higher intensity, before new positions are added. This places a premium on retention. Experienced employees are effectively carrying more of the operational load, and their continued engagement becomes a direct input to capacity. In practice, this elevates compensation reviews, development pathways and workload management from HR concerns to commercial considerations.

Sector Insights

Supply chain & logistics

The sector entered 2026 managing the same workforce challenges it has faced for several years. Driver shortages, an ageing operational workforce, and declining VET enrolments in logistics qualifications continue to constrain the candidate pipeline. IBIS World projects integrated logistics employment growing steadily through 2026, with average wages around $83,833 and profit margins near 7.3%.

The Iran conflict has changed the operating environment considerably. The closure of the Strait of Hormuz has rerouted Australian shipping through the Cape of Good Hope, adding 10 to 14 days to transit times, and emergency conflict surcharges of USD $1,500 to $4,000 per container are now live across Australian trade lanes. Fuel prices, already a material cost input, moved sharply during March. For a sector where purchases (mainly fuel) account for roughly 38% of revenue, the margin pressure is immediate.

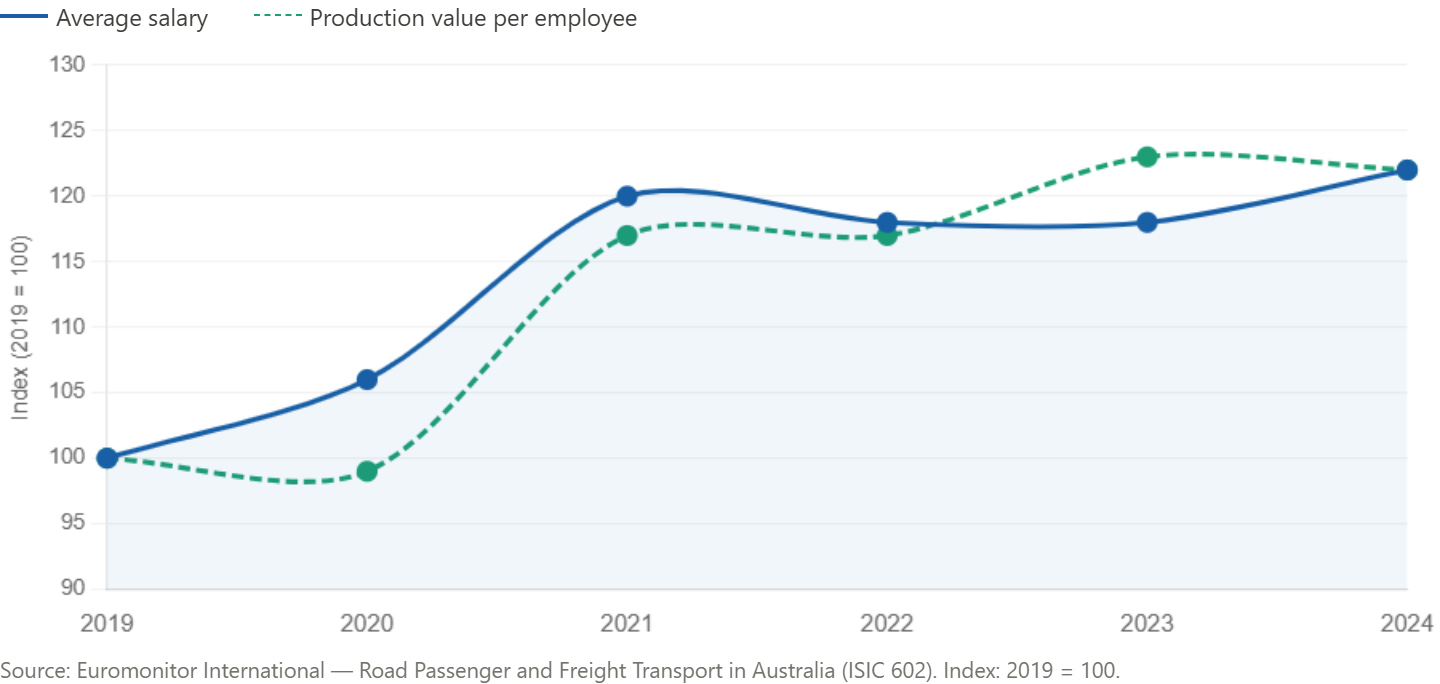

Cost structure over time, Road Transport, 2019–2024

The workforce implication runs counter to what the softer broader sentiment might suggest. Disruption tends to increase the value of operational and planning roles rather than reduce it. Freight forwarders who can manage rerouted carrier networks, supply chain coordinators capable of modelling inventory risk under volatile transit conditions, and transport managers who can renegotiate fuel cost exposure are all in acute demand. Euromonitor data for road transport shows that during the 2020 disruption, salaries rose 6% while productivity per employee fell 1%. It took three years for the two measures to reconverge. Firms that closed the gap fastest were those with experienced operational staff already in place.

Labour costs vs employee productivity, Road Transport, 2019–2024

For employers in this sector, the operational question is whether existing teams have the capacity to absorb current disruption. Reactive hiring during peak pressure is expensive and tends to produce weaker matches. Planning ahead while the market remains relatively balanced is a more efficient path to the same outcome.

Finance & accounting

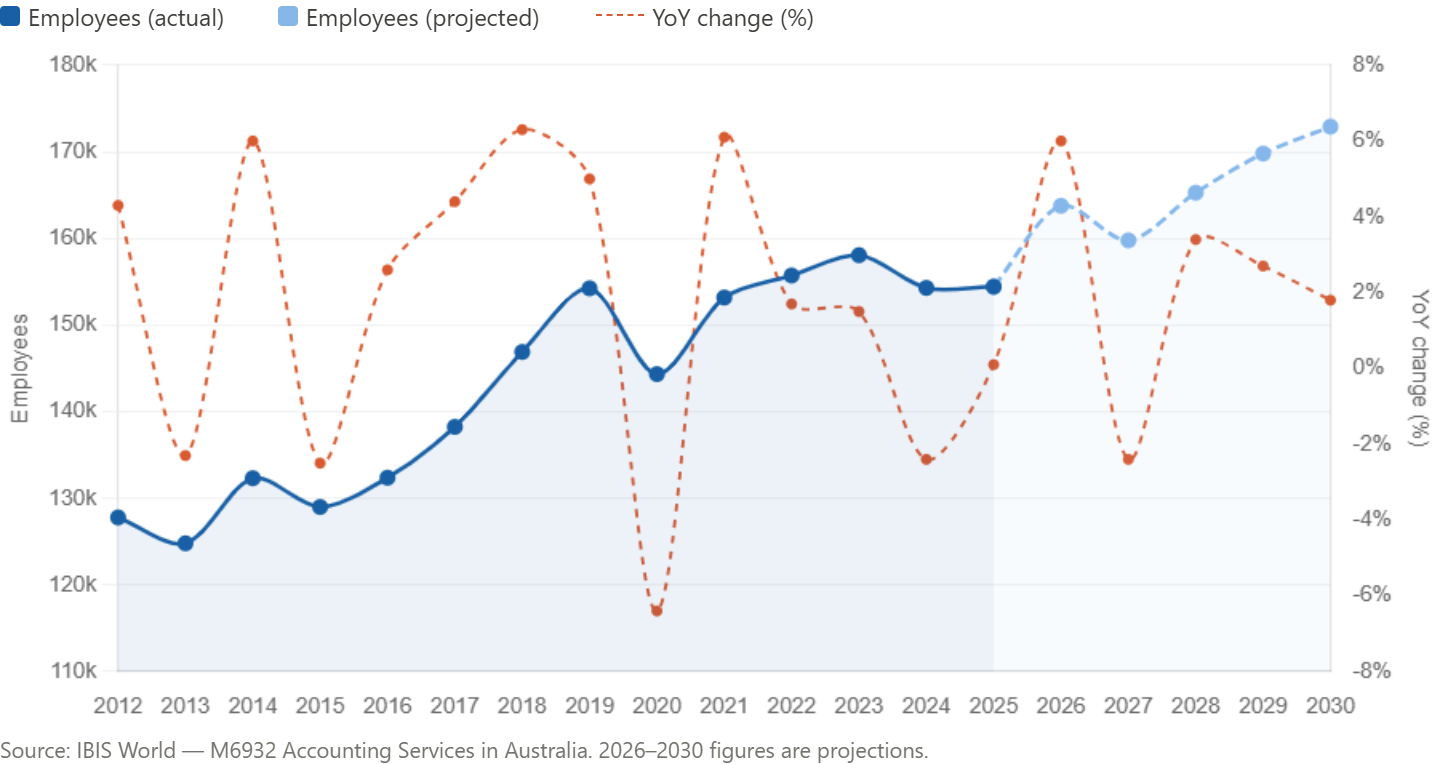

The accounting profession was already navigating a structural transition before the current geopolitical disruption added further complexity. IBIS World data shows the sector shed staff in 2024, with employee numbers falling 2.4% to around 154,000, then holding roughly flat in 2025. Projections point to a 6% rebound in 2026, though that forecast was set before Iran-related demand uncertainty emerged.

Accounting Services employees, 2012–2030

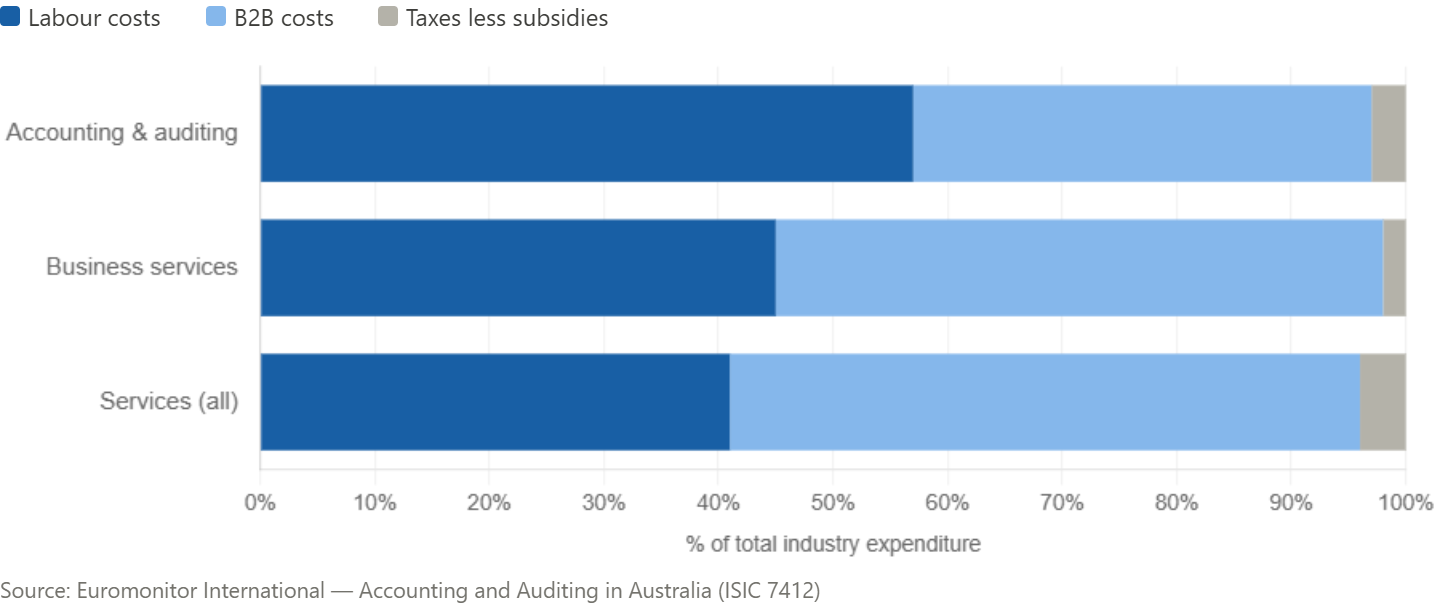

Two features of the sector make its workforce decisions commercially significant. First, accounting is unusually labour-intensive. Euromonitor data shows labour costs account for 57% of total expenditure in accounting and auditing, compared with 41% across services broadly. Second, firms that reduced headcount in 2024 continued to grow salaries. Average wages rose 4% that year despite falling employment, which indicates a deliberate shift toward fewer, more capable people rather than straightforward cost-cutting. The resulting workforce is smaller but more senior on average.

Cost structure comparison: Accounting vs Business Services vs Services

The profession itself is evolving faster than most. IBIS World and CPA Australia both identify the same direction of travel. Traditional compliance and transactional work is moving toward advisory services, data analysis, and business partnering. Technological proficiency, ESG capability, and commercial judgement are now weighted more heavily than pure technical accounting skills. This is part of why mid-level roles are taking longer to fill than they have in years. The work has changed faster than the supply of candidates has adapted.

The current environment reinforces that shift. Rising input costs, margin pressure, and more complex scenario planning have increased demand for finance professionals who can model risk and support commercial decisions. Industry data indicates roughly a third of accounting firms plan permanent hiring increases in 2026, while a similar share is expanding contractor and interim functions for project-based work. For employers, the competition is less about volume and more about securing commercial-minded finance capability, which is now the sector's scarcest resource.

Business support (HR & operations)

Business support functions are adjusting to a more demanding operating environment. Most Australian employers have indicated plans to recruit in 2026, though replacement hiring rather than expansion is the primary driver. The top priorities for the year are productivity and performance improvement, AI and digital upskilling, attracting talent, and workforce planning. Cost control sits below all of these, which indicates that workforce capability is being treated as a strategic investment rather than a discretionary expense even in a constrained environment.

HR and operations teams are also carrying a substantially heavier compliance load. The Cyber Security Act 2024, Right to Disconnect provisions, casual conversion rules, fixed-term contract limits, and emerging AI governance frameworks have collectively added material obligations over the past 18 months. AI adoption at work has become near-universal in office-based roles, but formal training lags behind considerably. Closing the gap between adoption and governance falls squarely on HR and operations functions.

Skills-based hiring has been steadily displacing traditional credentialing. Organisations report that hires assessed on demonstrated capability tend to outperform those assessed on qualifications alone. This is reshaping how business support roles are scoped, advertised, and filled. The practical effect is shorter shortlists, faster decisions, and a higher bar for what candidates can produce in the first weeks of a role. Within HR itself, demand is strongest for business partners, workforce planners, and employee relations specialists who can translate policy changes into operational practice.

Strategic Implications for Employers

Three observations stand out from the Q1 data.

The labour market entered the current period of uncertainty from a position of relative strength. Unemployment at 4.3%, employment at record levels, and participation above 66% all provide some buffer against the pressures building in forward-looking indicators. That buffer may narrow over the next two quarters, but it has not disappeared yet.

The compositional volatility between February and March suggests employers are still working out their preferred hiring mix. When conditions are uncertain and individual roles carry more weight, the accuracy of each hire matters more than the volume of hiring. This affects how roles are briefed, screened, and onboarded, and it raises the commercial cost of a poor fit.

Sector-specific shortages are structural rather than cyclical. Ageing workforces in logistics, the shift toward advisory capability in finance, and the expanding compliance remit in HR are not issues that resolve with the next upturn. These gaps persist through cycles and tend to be most acutely felt when operating conditions are hardest.

For employers working through this environment, the practical choices narrow. Reactive hiring during peak pressure is expensive, uncompetitive, and prone to mismatched outcomes. Investing in workforce capability while conditions are still relatively balanced, through targeted hiring, structured development, and deliberate retention, is a more economical route to the same result. Employers that treat workforce capability as part of commercial resilience, rather than an overhead to be minimised, tend to be better placed when the operating environment tightens.

If you would like to get in touch, email us at jobs@alexanderappointments.com.au or call us on 02 9659 4411.

Ready to start the journey?

Search positions or find talent online, or get in touch with us via email. We can’t wait to meet